The board of directors approved the following second quarter dividends for both the membership capital stock (Class A) and activity-based capital stock (Class B) at its June 27, 2024, meeting:

- Class A Common Stock: 4.75 percent (per annum)

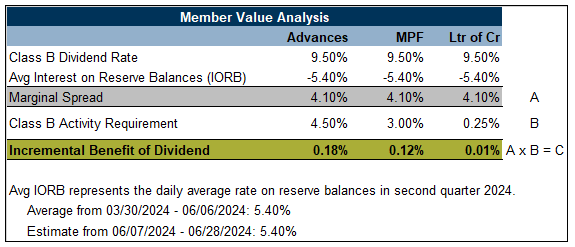

- Class B Common Stock: 9.50 percent (per annum)

We are pleased to provide continued strong returns on your investment in your cooperative to help build your communities. The table below illustrates the incremental benefit you receive from the Class B Stock dividend as you use each of our three main products – advances, the Mortgage Partnership Finance® (MPF®) Program and letters of credit.

FHLBank Topeka balances maintaining strong capital growth, offering liquidity to members at competitive rates and providing an attractive return on activity-based stock. Based on current market expectations of short-term interest rates, we anticipate paying dividend rates in ranges between 4.50 to 5.00 percent for Class A and 9.25 to 9.75 percent for Class B for the third quarter.

Over time, our dividend rates have moved directionally with short-term interest rates but given the nominal level of rates, our ability to further increase dividend rates may be limited. Please keep in mind that market conditions and movements in short-term interest rates can be unpredictable. Adverse changes in FHLBank’s financial results may result in lower dividend rates in future quarters than we currently anticipate paying.

Please contact the Lending Desk or your regional account manager with your questions on the positive impact of the above-market Class B dividend on FHLBank advance rates, letter of credit costs and MPF mortgage loan sales. They can help compare the all-in cost of advances to various deposit pricing strategies and purchased deposit funding options.

The dividends on both classes of stock are payable in the form of Class B Common Stock and will be credited to your institution’s capital stock account at the close of business on June 28, 2024. Any partial shares will be paid in cash and credited to your institution’s demand deposit account on that date as well.

If you have any questions related to the dividend, please contact the Lending Desk at 800.809.2733. We appreciate your continued partnership.

“Mortgage Partnership Finance” and “MPF” are registered trademarks of the Federal Home Loan Bank of Chicago.

The information contained in this announcement contains forward-looking statements within the meaning of the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements include statements describing the objectives, projections, estimates or future predictions of FHLBank’s operations. These statements may be identified by the use of forward-looking terminology such as “anticipates,” “believes,” “may,” “is likely,” “could,” “estimate,” “expect,” “will,” “intend,” “probable,” “project,” “should” or their negatives or other variations on these terms. FHLBank cautions that by their nature forward-looking statements involve risks or uncertainties and that actual results may differ materially from those expressed in any forward-looking statements as a result of such risks and uncertainties, including but not limited to: changes in the general economy and capital markets, the rate of inflation or deflation, employment rates, housing market activity and pricing, the size and volatility of the residential mortgage market, geopolitical events, and global economic uncertainty; political events, including legislative, regulatory, judicial, or other developments that affect FHLBank; its members, counterparties or investors in the consolidated obligations of the FHLBanks, such as any government-sponsored enterprise (GSE) reforms, any changes resulting from the Federal Housing Finance Agency’s (FHFA) review and analysis of the FHLBank System, including recommendations published in its “FHLBank System at 100: Focusing on the Future” report, changes in the Federal Home Loan Bank Act of 1932, as amended (Bank Act), changes in applicable sections of the Federal Housing Enterprises Financial Safety and Soundness Act of 1992, or changes in other statutes or regulations applicable to the FHLBanks; external events, such as economic, financial, or political disruptions, and/or wars, pandemics, and natural disasters, including disasters caused by climate change, which could damage our facilities or the facilities of our members, damage or destroy collateral pledged to secure advances or mortgages held for portfolio, which could increase our risk exposure or loss experience; effects of derivative accounting treatment and other accounting rule requirements, or changes in such requirements; competitive forces, including competition for loan demand, purchases of mortgage loans and access to funding; the ability of FHLBank to introduce new products and services to meet market demand and to manage successfully the risks associated with all products and services; changes in demand for FHLBank products and services or consolidated obligations of the FHLBank System; membership changes, including changes resulting from member failures or mergers, changes due to member eligibility, or changes in the principal place of business of members; changes in the U.S. government's long-term debt rating and the long-term credit rating of the senior unsecured debt issues of the FHLBank System; soundness of other financial institutions, including FHLBank members, non-member borrowers, counterparties and the other FHLBanks; the ability of each of the other FHLBanks to repay the principal and interest on consolidated obligations for which it is the primary obligor and with respect to which FHLBank has joint and several liability; the volume and quality of eligible mortgage loans originated and sold by participating members to FHLBank through its various mortgage finance products; changes in the fair value and economic value of, impairment of, and risks associated with FHLBank’s investments in mortgage loans and mortgage-backed securities or other assets and the related credit enhancement protections; changes in the value or liquidity of collateral underlying advances to FHLBank members or nonmember borrowers or collateral pledged by reverse repurchase and derivative counterparties; volatility of market prices, changes in interest rates and indices and the timing and volume of market activity, including the effects of these factors on amortization/accretion; gains/losses on derivatives or on trading investments and the ability to enter into effective derivative instruments on acceptable terms; changes in FHLBank's capital structure; FHLBank's ability to declare dividends or to pay dividends at rates consistent with past practices; the ability of FHLBank to keep pace with technological changes and innovation such as artificial intelligence, and the ability to develop and support technology and information systems, including the ability to manage cybersecurity risks and securely access the internet and internet-based systems and services, sufficient to effectively manage the risks of FHLBank's business; and the ability of FHLBank to attract and retain skilled individuals, including qualified executive officers. Additional risks that might cause FHLBank’s results to differ from these forward-looking statements are provided in detail in FHLBank’s filings with the SEC, which are available at www.sec.gov.